Are you curious about the current investment property mortgage rates and how they impact your real estate investment? Understanding these rates is essential to maximizing your investment returns. In today’s dynamic market, rates can fluctuate, influencing borrowing costs and overall profitability.

In this blog, we’ll compare the latest investment property mortgage rates and explain the factors that affect them. I will also offer some tips for getting the best deal.

By the end, you’ll clearly understand how to plan your next investment wisely. Stay with me to gain valuable insights that could save you thousands on your next property deal.

Dive Deeper into Your Real Estate Potential: As the founder and CEO of eFunder, I bring my extensive experience in real estate and commercial mortgages to enhance your investment strategy. Stay tuned for actionable insights, and don’t miss the exclusive offer at the end of this article, designed to revolutionize your lead generation approach.

Current Mortgage Rates for Investment Property

Diving into mortgage rates can feel like chasing a shadow—those numbers keep dancing around. For real estate investors, staying informed about these fluctuations is crucial. Even a tiny percentage bump can nudge your monthly budget over the edge.

But why do these rates fluctuate? Several factors come into play. Economic indicators like inflation and unemployment rates heavily influence mortgage rates.

When the economy is strong, rates tend to rise. During economic downturns, rates usually fall.

What type of loan is best for investment property?

Choosing the right mortgage loan for your investment property is essential. Here are several types of loans to consider.

Fixed-Rate Mortgages

Fixed-rate mortgages are a popular choice for real estate investors. They provide a stable interest rate and consistent monthly mortgage payments throughout the loan term, making budgeting simpler.

Adjustable-Rate Mortgages (ARMs)

Adjustable-rate mortgages (ARMs) have interest rates that change over time. They often start with a lower rate, which can increase later. This type of loan can be beneficial if you plan to sell or refinance before the rate adjusts.

Interest-Only Loans

Interest-only loans allow you to pay just the interest for a certain period of time. This can lower your initial payments, but you must start paying the principal later. Investors use these loans to sell the property before the principal payments begin.

Portfolio Loans

Portfolio loans are another option. The lender holds these instead of selling them on the secondary market. They can offer more flexibility in terms of terms and approval criteria, making them suitable for unique investment properties.

Understanding these loan types helps you make the best choice for your investment strategy. Each has its own benefits and risks, so consider your long-term goals and financial situation before deciding.

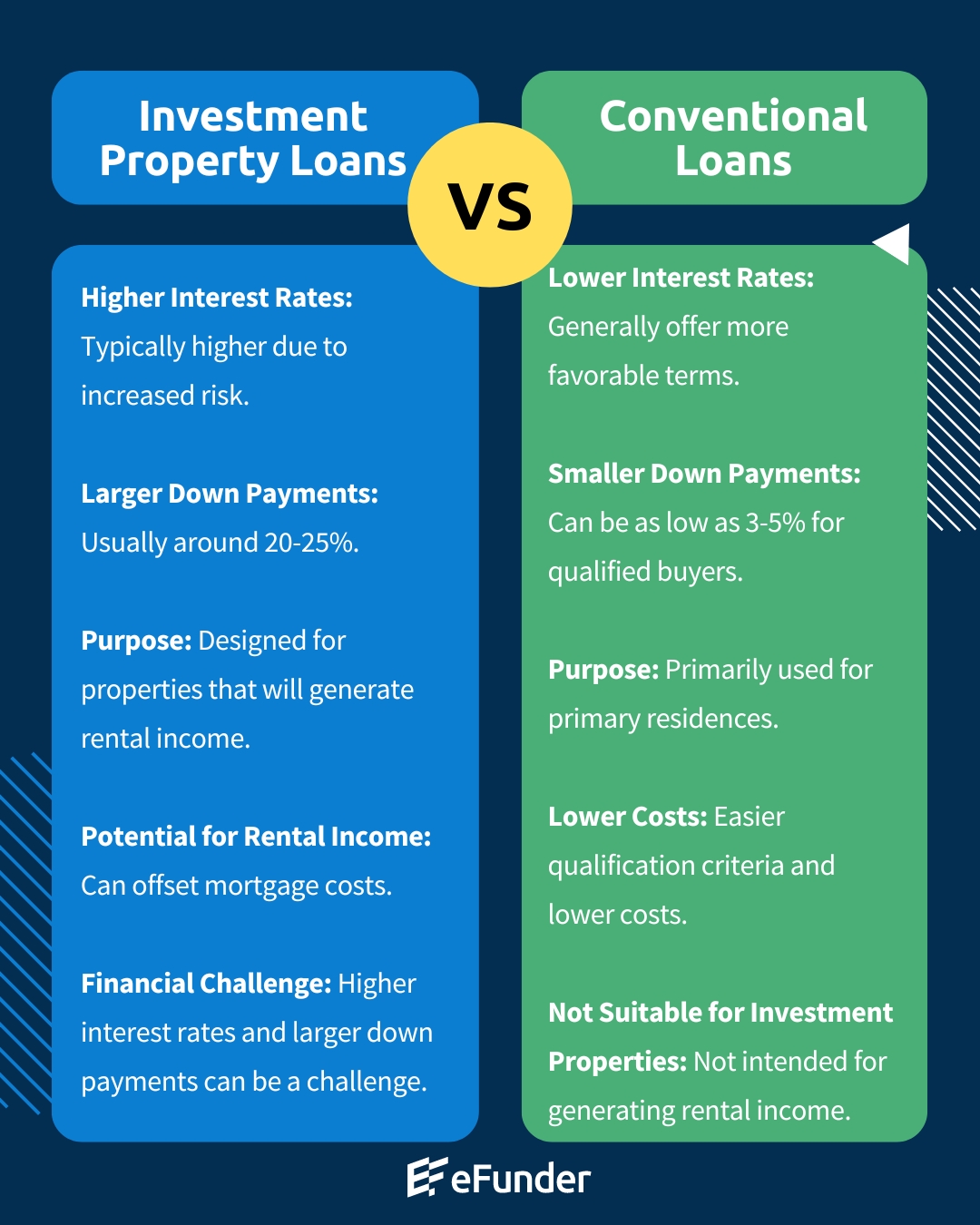

Investment Property Loans vs. Conventional Loans

Understanding the differences between investment property loans and conventional loans is crucial for investors. Both have unique features, benefits, and drawbacks.

When deciding between the two, consider your financial situation and investment goals. Understanding these differences helps you choose the best loan type for your needs.

30-Year Mortgage Rates for Investment Properties

A 30-year mortgage is a popular choice for investment properties. This loan has a fixed interest rate. The monthly payments also stay the same for 30 years. This makes it easier to plan for the long term.

One major advantage of a 30-year mortgage is lower monthly payments compared to shorter-term loans. Spreading payments over 30 years makes it easier to manage cash flow. This can be especially beneficial for rental properties, allowing for better budgeting and potentially higher profit margins.

However, it’s important to note that 30-year mortgages typically have higher interest rates than shorter-term loans. Over time, you may pay more in interest than a 15-year mortgage. Despite this, the lower monthly payments often make them a preferred option for many investors.

When comparing loan terms, consider your investment strategy. A 15-year mortgage will have higher monthly payments but lower overall interest costs. A 30-year mortgage offers smaller payments but higher interest over time.

How Much Down for Investment Property?

The down payment is a key factor when buying an investment property. Typically, lenders require a down payment of 20–25% of the property’s purchase price. This is higher than the down payment for a primary residence, which can be as low as 3-5%.

A larger down payment reduces the lender’s risk. It can also help you get better loan terms and lower interest rates. To save for a down payment, set aside some of your rent money. You can also look into programs that assist with down payments if you own other properties.

How to Get a Loan for Investment Property

Securing a mortgage for an investment property involves several steps. First, check your credit score. A higher score can help you get better loan terms. Next, save for the down payment, aiming for at least 20–25%.

Then, gather your financial documents. Lenders want to see proof of income, tax returns, and bank statements. Research and compare lenders to find the best rates and terms. Consider getting pre-approved to show sellers you are a serious buyer.

Finally, submit your application and await approval. Follow these steps and prepare well to increase your chances of getting a loan for your investment property.

Pros and Cons of Investment Property Mortgages

Understanding the pros and cons of investment property mortgages is essential for investors. Here’s a concise comparison to help you weigh your options:

Pros

- Potential for Rental Income: Investment properties can generate steady rental income, helping to cover mortgage payments and other expenses.

- Appreciation: Over time, property values may increase, providing significant returns on investment.

- Tax Benefits: Investors can often deduct mortgage interest, property taxes, and other expenses from their taxable income.

- Diversification: Real estate diversifies your investment portfolio, spreading risk across different asset types.

Cons

- Higher Interest Rates: Investment property mortgages usually come with higher interest rates compared to primary residence loans.

- Larger Down Payments: Lenders often require a down payment of 20–25%, which can be a significant financial commitment.

- Maintenance and Management: Managing rental properties can be time-consuming and may require dealing with repairs and tenant issues.

- Market Risk: Real estate markets can be volatile, and property values can decrease, impacting your investment.

How to Get the Best Investment Property Mortgage Rates

Securing the best mortgage rates for your investment property can save you thousands of dollars. Here are some strategies to help you get the best deal.

- First, improve your credit score. Lenders offer better rates to borrowers with high credit scores. Pay off debts and keep your credit utilization low.

- Next, save for a larger down payment. A 20–25% down payment can help you secure lower interest rates. It also reduces the lender’s risk, making you a more attractive borrower.

- Shop around and compare offers from different lenders. Interest rates and terms can vary, so it’s essential to get quotes from multiple sources. Feel free to negotiate for better terms.

- Consider working with a mortgage broker. Brokers have access to various lenders and can help you find the best rates and terms for your situation.

- Lastly, choose the right loan type. Fixed-rate mortgages offer stability with consistent payments, while adjustable-rate mortgages may offer lower initial rates.

By following these strategies, you can secure the best mortgage rates for your investment property. This will help you maximize your returns and achieve your financial goals.

Conclusion

Navigating property mortgage rates can feel like a maze. Staying on top of mortgage trends is crucial. Whether you’re comparing rates for your first home loan or considering refinancing for an investment, expert advice is essential.

Each financial decision can impact your future. Monitoring these details ensures smarter and more rewarding outcomes. Start transforming your real estate dreams into reality with eFunder. Schedule a FREE consultation today and discover how we can help you secure the best financing for your next investment. Let’s build your success story together!

Additionally, don’t miss out on our exclusive offer – a 30-day free trial from Realeflow, specifically tailored for ambitious investors like you.

Some of the links in this article may be affiliate links, which can compensate us at no cost if you decide to purchase. This blog is not intended to provide financial advice.