Credit score often becomes a point of concern when investors look into DSCR loans.

Even though these loans are primarily based on property income, credit still plays a role in how a deal is evaluated and structured. Many investors are unsure how much it actually matters or where they stand.

This article looks at how minimum credit score comes into play in real DSCR loan scenarios, and what investors can expect depending on their profile.

How Minimum Credit Score Impacts DSCR Loan Structure

A minimum credit score is not just a pass or fail requirement. It directly affects how a deal is structured.

In most DSCR scenarios, credit score influences three key areas:

• loan to value

• interest rate range

• reserve requirements

For example, an investor with a higher credit score may qualify for a higher leverage position. This means a lower down payment relative to the property value.

On the other hand, a lower credit score does not always disqualify a deal. It may simply require adjustments such as more equity, stronger cash flow, or additional reserves.

This is an important distinction. DSCR loans are flexible, but that flexibility depends on how the full deal profile comes together.

For a broader explanation of how DSCR loans work overall, this ties directly into the main authority page on DSCR loans for real estate investors.

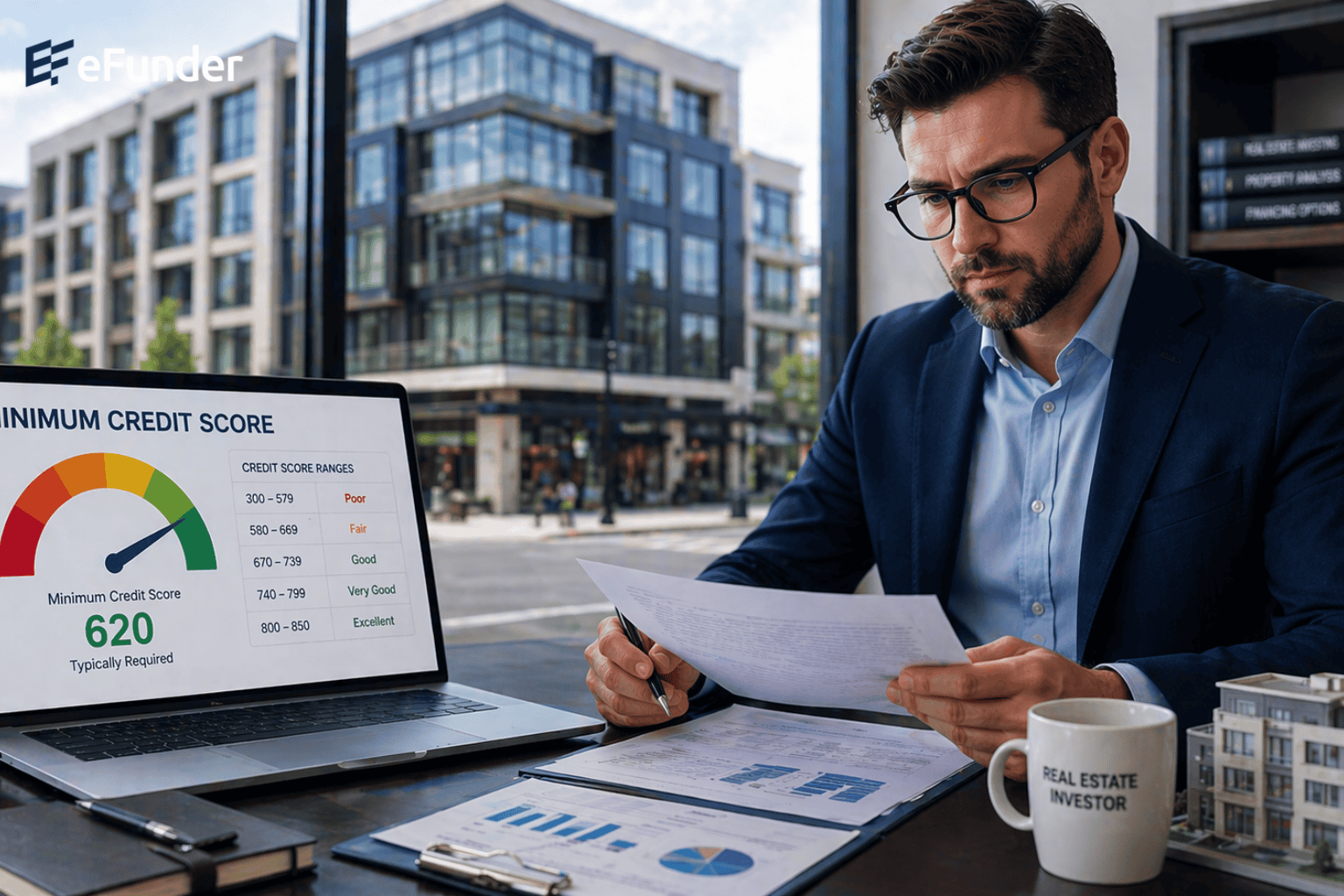

How Credit Score Ranges Affect DSCR Loan Options

Instead of thinking in terms of one minimum number, it is more useful to think in ranges.

680 and above

This is typically considered a strong credit profile for DSCR loans. Investors in this range often have access to more competitive structures and smoother approvals.

640 to 679

This is a common middle range. Many investors operate here, especially those actively scaling portfolios. Deals can still work well, but may require slightly more conservative terms.

620 to 639

This is where structure becomes more important. Investors may still qualify, but lenders will look more closely at:

• property cash flow

• experience level

• liquidity

Below 620

Deals become more situational. Some scenarios may still work, but they often require strong compensating factors such as low leverage or a high-performing property.

The key takeaway is that credit score works in combination with the deal, not in isolation.

Real Scenario Breakdown

Consider two investors looking at similar rental properties.

Investor A

• Credit score: 705

• Purchase price: $400,000

• DSCR: 1.25

This investor may be able to secure higher leverage and more flexible terms because the credit profile supports the overall deal strength.

Investor B

• Credit score: 635

• Purchase price: $400,000

• DSCR: 1.25

The property performs the same, but the structure may change. This investor might need:

• a larger down payment

• additional reserves

• slightly adjusted loan terms

The deal can still work, but the path to approval is different.

This is where working with a financing platform like eFunder Capital becomes important. The role is not just to find a loan, but to structure the deal based on the full profile of the borrower and property.

Common Credit Score Mistakes Investors Make

One common mistake is assuming that a single credit score number determines eligibility.

In reality, lenders evaluate the full credit profile. This includes:

• payment history

• outstanding debt

• recent credit activity

Another mistake is waiting to improve credit before pursuing a deal. In some cases, the deal itself may still be viable with adjustments to structure.

A third issue is focusing only on credit score while ignoring property performance. In DSCR lending, the income of the property is often just as important as the borrower profile.

Investors who understand this balance tend to move more efficiently when structuring deals.

Final Thoughts

Minimum credit score in DSCR loans is not a strict cutoff. It is a variable that affects how the deal is structured.

Higher scores generally create more flexibility. Lower scores do not eliminate opportunities, but they require stronger supporting factors.

The most effective approach is to evaluate the full scenario, including credit, property income, and investment strategy.

If you have a deal you would like reviewed, submit it here:

https://efundercapital.com/deal-intake