Are you considering investing in commercial real estate in Pittsburgh, PA, but feeling overwhelmed by the various financing options? Navigating commercial mortgages can be complex due to the multiple terms, rates, and conditions involved.

This comprehensive guide will help you understand the different financing options for commercial real estate in Pittsburgh, PA, from traditional bank loans to innovative options like bridge loans. By the end of this post, you’ll have the confidence and clarity to choose the right financing for your next real estate investment in Pittsburgh.

- A commercial mortgage is a loan secured by commercial property, offering significant capital and flexible options like cash-out refinancing.

- Commercial mortgage rates range from 5.61% to 8.01% as of May 2024, typically higher than residential rates by 0.25% to 0.75%.

- Types of commercial loans include bridge loans (short-term), commercial mortgage loans (long-term), and CMBS loans (bundled for diversification).

- A strong credit history is crucial for favorable loan terms; lenders assess credit scores and property income potential.

- Choosing the right lender involves comparing rates, understanding business goals, reading reviews, checking for hidden fees, and building trust.

What Is A Commercial Mortgage?

A commercial mortgage, also known as a commercial real estate loan, is a loan secured by commercial or residential investment property.

These loans offer investors access to significant capital, crucial for handling significant investments, such as multi-level office complexes or expansive shopping centers. Unlike traditional 30-year residential property mortgages, commercial mortgages offer a 20-25-year term.

Additionally, business owners and investors in Pittsburgh can work with mortgage lenders to buy commercial properties directly. They can also opt for a cash-out refinance on an existing commercial mortgage loan, allowing them to use their equity for additional property purchases or working capital purposes.

However, each lender offers different loan programs. So do your homework to ensure the loan terms align with your business plan.

Current Commercial Mortgage Rates and What You Need to Know

As of May 23, 2024, Freddie Mac loans have commercial mortgage rates ranging between 5.61% and 6.39%-8.01% (source). While Fannie Mae loans range from 6.49% to 7.81%, HUD 223(f) loans vary from 6.25% to 7.30%, and CMBS loans fluctuate between 6.46% and 7.95%.

Generally, commercial mortgage interest rates are about 0.25% to 0.75% higher than residential mortgages. For more detailed information, visit our post on Commercial Mortgage Rates.

Types of Commercial Loans

Several financing options are available when exploring commercial mortgages in Pittsburgh. Understanding these options is crucial when choosing the right investment.

Bridge Loans

Bridge loans are a type of short-term financing that provides quick access to funds. They bridge the gap between the purchase of an investment and its subsequent refinancing.

Bridge loans are ideal for Pittsburgh investors who need to purchase a property quickly but have to sell their existing one. However, because of their short duration and quick access to funds, these loans have higher interest rates.

Commercial Mortgage Loans

Commercial mortgage loans secure the property, offering a stable, long-term financing solution. Lenders typically structure these loans with terms of up to 20 or 30 years, offering consistent commercial mortgage rates.

These loans provide stable financing suitable for investors who plan to hold a property for an extended period.

Commercial Mortgage-Backed Securities (CMBS)

Commercial mortgage-backed securities (CMBS) combine multiple loans. These bundles are sold as bonds to investors on the secondary market.

This will allow lenders to free up capital and offer new loans. CMBS loans provide an excellent opportunity for investors who want to diversify their portfolios with commercial real estate.

The Role of Credit in Securing a Commercial Mortgage

Your credit history is important when you apply for a commercial mortgage in Pittsburgh. It acts like a financial report card that shows lenders how well you’ve handled your debt before.

A strong credit score means you’re good at managing debt, which can get you better loan terms, like lower interest rates. However, if your credit score is lower, you might face higher interest rates and stricter conditions.

Lenders also assess whether your purchased property will generate enough income to cover the mortgage, taxes, and insurance. They assess financial viability using debt service coverage ratios and loan-to-value ratios.

Tips to Improve Your Credit

Here’s how you can make your credit look better before applying:

eFunder Capital specializes in funding solutions for borrowers in Pittsburgh who don’t qualify for traditional bank financing.

Collateral in Commercial Mortgages

In commercial mortgages, collateral is like a safety net, providing security amid financial risks. Generally, the property you’re buying acts as collateral. This helps lenders feel secure, allowing them to offer you better terms like lower interest rates and loan limits.

If you fail to meet the loan payments, the lender can take ownership of the property. To improve your chances of getting a loan, ensure the property can generate consistent income.

Moreover, it can be upgraded to increase its value and pay off any debts tied to it. Keeping your collateral secure is crucial for financial stability.

How to Choose the Right Commercial Mortgage Lender

Selecting the right lender for your commercial mortgage is the first step in ensuring your business’s financial success. Here is a guide to help you choose the right lender in Pittsburgh, PA.

- Interest Rates: Check if the lender offers fixed or variable rates and compare these to ensure they are competitive.

- Understanding Your Business: Choose a lender who understands your business goals. A lender who aligns with your vision can offer tailored services that benefit your long-term plans.

- Read Customer Reviews: Look at what other customers say about their experiences with the lender. These reviews can provide valuable insights into the lender’s service quality and reliability.

- Check for Hidden Fees: Ensure the lender is transparent about all costs. Hidden fees can be an unpleasant surprise, so choose a lender that’s open about their charges.

- Compatibility and Trust: Choose a lender you can trust. You’ll be collaborating for the long term, so you need a compatible, trustworthy partner who understands your business needs.

Take your time to evaluate all these factors carefully. The right commercial mortgage lender is not just a financial provider but a partner in your business journey.

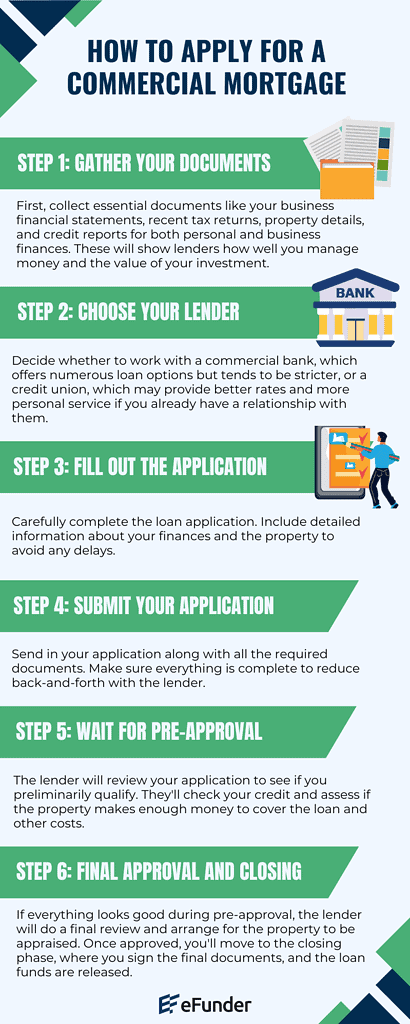

How to Apply for a Commercial Mortgage

Applying for a commercial mortgage might seem tricky, but you can make it smooth and straightforward with a clear plan. Here’s an easy-to-follow guide to help you through the application process.

For more detailed steps and tips, check out our How to Apply for a Commercial Mortgage.

FAQs about Commercial Mortgages

What are typical terms for a commercial mortgage?

Commercial mortgage loans typically last 5 to 20 years. However, if the loan is not fully paid off by the end of the term, a balloon payment is incurred.

How do I prepare for a commercial loan?

Prepare your financial documents and draft a solid business plan. Ensure that you select a prime property as well.

What credit score do you need for a commercial mortgage?

To qualify for a commercial mortgage, a credit score of at least 680 is recommended. However, lenders also evaluate other factors, such as your business income, the value of the collateral, and your overall financial health. Improving your credit score can significantly enhance your chances of securing favorable loan terms.

What do banks look for in commercial loans?

Banks evaluate potential borrowers based on their credit history, cash flow, collateral value, and business plan.

Conclusion

Understanding commercial property mortgages is crucial for making informed investment decisions in Pittsburgh. Ensure your important documents are ready when you apply, and choose a lender that understands the unique dynamics of Pittsburgh’s commercial real estate market. Remember, alternative lending options are also available, each with its own advantages and disadvantages, tailored to meet the specific needs of Pittsburgh investors.

Your journey into Pittsburgh’s commercial real estate doesn’t end here. Continue to explore and deepen your knowledge to make the most of the opportunities available in this vibrant city. Are you ready to leverage the best opportunities in Pittsburgh’s commercial real estate?

Take the next step with eFunder. Schedule a FREE consultation today to explore our tailored loan programs and receive expert guidance and strategic financing solutions. Schedule Now!

Additionally, don’t miss out on our exclusive offer – a 30-day free trial from Realeflow, specifically tailored for ambitious investors like you. Click here to seize this opportunity and elevate your investment strategies.

Some of the links in this article may be affiliate links, which can compensate us at no cost if you decide to purchase. This blog is not intended to provide financial advice.