DSCR loans are commonly used by real estate investors to finance rental properties. Unlike conventional mortgages, these loans are primarily evaluated based on the income generated by the property rather than the borrower’s personal income.

For many investors, DSCR financing creates opportunities to expand a rental portfolio more efficiently. At the same time, these loans also come with tradeoffs that should be understood before using them as part of a long-term investment strategy.

The advantages and disadvantages of DSCR loans often become more noticeable as leverage increases. Investors may be able to acquire more properties with less capital, but higher leverage can also reduce cash flow flexibility and increase overall portfolio risk.

Understanding both sides of the structure is important when evaluating rental property financing options.

What Is a DSCR Loan?

A DSCR loan is a type of investment property financing that focuses on the property’s debt service coverage ratio rather than the borrower’s personal debt-to-income ratio.

The lender reviews whether the rental income generated by the property is sufficient to cover the proposed loan payment and operating expenses.

In general, properties with stronger cash flow are more likely to meet DSCR requirements.

These loans are frequently used for:

- single-family rental properties

- small multifamily properties

- mixed-use properties

- portfolio expansion strategies

Why Investors Use DSCR Loans

One reason investors use DSCR loans is flexibility.

Traditional financing can become restrictive as investors acquire more properties. Personal income documentation and debt-to-income calculations may limit future borrowing capacity even when the investment properties themselves perform well.

DSCR financing approaches the deal differently by focusing on the asset and its rental income.

For mortgage brokers and financing platforms like eFunder Capital, DSCR loans also create additional flexibility when structuring investor financing scenarios.

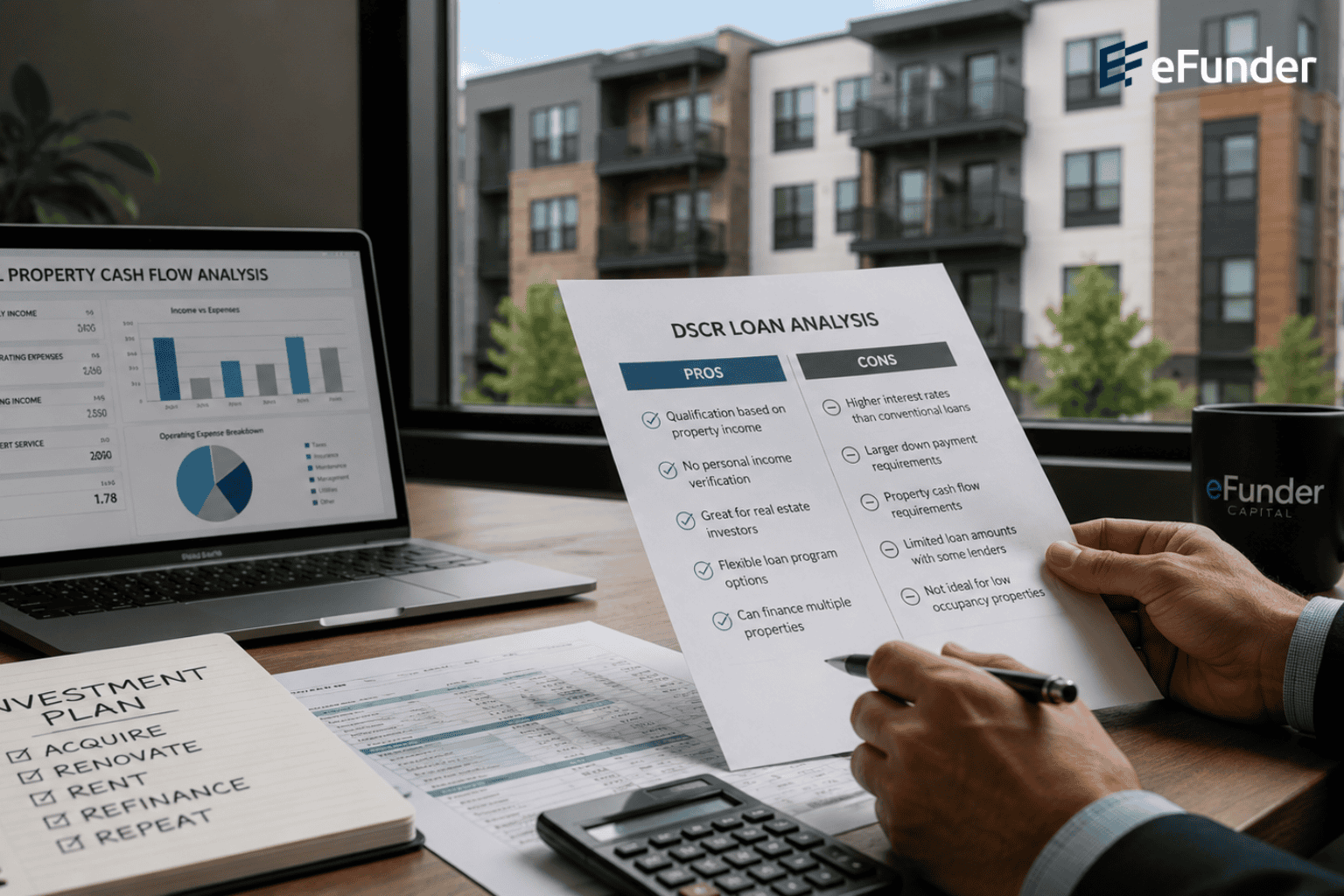

Advantages of DSCR Loans

Qualification Based on Property Income

One of the primary advantages of DSCR loans is that qualification is centered around rental income rather than personal employment income.

This can benefit investors who:

- own multiple properties

- write off significant business expenses

- operate through investment entities

- have complex tax returns

If the property generates sufficient income to support the proposed debt payment, the deal may qualify even when traditional income documentation would be difficult.

Ability to Scale a Portfolio

DSCR loans are commonly used by investors who want to expand their rental portfolio over time.

For example, an investor using lower down payments may be able to acquire two or three rental properties instead of one larger purchase.

This strategy can accelerate portfolio growth when properties are selected carefully and cash flow remains stable.

Simplified Underwriting Process

The lender primarily evaluates:

- rental income

- property cash flow

- property condition

- credit profile

- reserve requirements

Because extensive personal income documentation is often reduced, experienced investors may find the process more efficient.

In competitive acquisition markets, speed and simplicity can become important advantages.

Disadvantages of DSCR Loans

Higher Interest Rates

One potential downside of DSCR loans is that interest rates are often higher than traditional conventional financing.

Since these loans are designed for investment properties and rely heavily on property performance, pricing may reflect additional risk from the lender’s perspective.

Over time, a higher interest rate can reduce monthly cash flow and increase the overall cost of financing.

Reduced Cash Flow at Higher Leverage

As leverage increases, debt service also increases.

While higher leverage can reduce the amount of upfront capital required, it may also leave less remaining cash flow after expenses and loan payments.

A property may still meet minimum DSCR requirements while producing tighter monthly margins in practice.

This can make it more difficult to absorb:

- maintenance expenses

- vacancy periods

- property management costs

- insurance increases

- unexpected repairs

Increased Exposure to Market Changes

Properties operating with tighter DSCR margins may become more sensitive to shifts in rental markets or operating costs.

For example, a temporary vacancy or decline in rental income may have a larger impact when debt obligations are already high.

This becomes more important when multiple properties within a portfolio are financed with similar leverage structures.

The strategy itself is not necessarily problematic, but it requires stronger planning, reserves, and underwriting discipline.

Example Scenario

Consider a rental property generating $3,200 per month in rent.

Moderate Leverage Example

- Loan amount: $260,000

- Monthly debt service: approximately $1,900

This structure leaves additional room for operating expenses while still producing stable monthly cash flow.

Higher Leverage Example

- Loan amount: $320,000

- Monthly debt service: approximately $2,400

In this scenario, the investor uses less upfront capital but operates with a smaller cash flow margin.

The property may still qualify under DSCR guidelines, but the deal has less flexibility if expenses rise or vacancy occurs.

This illustrates one of the main tradeoffs associated with DSCR financing. Higher leverage can support faster portfolio growth, but it also increases sensitivity to changes in property performance.

Common Mistakes Investors Make

One common mistake is focusing only on minimum DSCR qualification thresholds.

A property may technically qualify while still operating with very limited cash flow after realistic expenses are considered.

Another issue is underestimating operating costs. Investors should account for:

- maintenance

- vacancy

- property management

- insurance

- capital expenditures

Market selection also matters. Properties in unstable rental markets may carry greater risk when combined with aggressive leverage structures.

More conservative underwriting assumptions can help reduce long-term portfolio stress.

Final Thoughts

DSCR loans provide real estate investors with a flexible financing option for acquiring and scaling rental properties. Qualification based on property income can create opportunities that may not fit traditional lending guidelines.

At the same time, DSCR financing also involves tradeoffs. Higher leverage can reduce cash flow margins and increase sensitivity to vacancy, expenses, and market changes.

If you have a deal you would like reviewed, submit it here: