So, you’ve stumbled upon the ultimate project home. It has great potential, but it needs some serious renovation. The only problem? You don’t have the cash to buy the home and pay for all the repairs it needs. That’s where the rehab loans come to the rescue. So, what is rehab loan? A rehab loan is a special type of financing designed specifically for buyers who want to purchase a home that needs work.

With a rehab loan, you can roll the cost of renovations into your mortgage, so you only have one loan to worry about. Sounds pretty good, right? Let’s take a closer look at what is a rehab loan and how it works.

What is a Rehab Loan?

A rehab loan is a loan that homeowners and investors use to finance the acquisition and renovation of a home, often as a residence. Rehab loans are ideal because they combine acquisition and rehab financing into a single loan, making it a fast and easy way for investors to finance a project.

Rehab loans are designed to help people buy and fix up a home. The loan allows homebuyers to pay for the purchase of and repairs to the house, helping them meet their needs without spending too much money.

Types of Rehab Loans

There are several types of rehab loans available, each with its own set of requirements and benefits. Some of the most common types include:

- FHA 203(k) loans

- Fannie Mae HomeStyle Renovation Mortgage

- Freddie Mac CHOICERenovation Loan

- Conventional rehab loans

Each of these loan options has its own set of eligibility requirements, loan limits, and renovation guidelines. It’s important to research and compare the different options to find the one that best suits your needs.

How Rehab Loans Work

The process for getting a rehab loan is similar to that of any other home loan. To qualify, borrowers start by completing a standard loan application and providing information and documentation about their finances, plus information about the property and project they want to finance.

The lender then reviews the application, evaluates the property, and determines whether the borrower qualifies. Once approved, the borrower obtains an initial loan amount based on the loan program’s requirements, allowing them to purchase or refinance the home and make repairs or improvements as part of their mortgage payment through a single transaction.

Benefits of Rehab Loans

One of the main benefits of rehab loans is that they provide funds for both the purchase and renovation of a property. This can be especially helpful for homebuyers who want to purchase a fixer-upper but don’t have the cash on hand to cover the renovation costs.

Rehab loans can also help homeowners save money by allowing them to finance the cost of repairs and upgrades into their mortgage, rather than paying for them out of pocket. This can be a more affordable option, especially for larger projects that require significant upfront costs.

How to Qualify for a Rehab Loan

Qualifying for a rehab loan is similar to qualifying for a traditional mortgage. Lenders will consider factors such as your credit score, income, debt-to-income ratio, and the value of the property you want to purchase or refinance.

Credit Score Requirements

Most rehab loans require a minimum credit score of 500 to 620, depending on the specific loan program. However, some lenders may have higher credit score requirements, so it’s important to look around and compare your options.

If your credit score is on the lower end, you may still be able to qualify for a rehab loan, but you may need to provide additional documentation or have a higher down payment.

Income and Debt Requirements

In addition to your credit score, lenders will also consider your income and debt-to-income ratio when determining your eligibility for a rehab loan. Most lenders require a debt-to-income ratio of 50% or less, meaning your monthly debt payments should not exceed 50% of your monthly income.

You’ll also need to provide documentation of your income, such as pay stubs, tax returns, and bank statements. Lenders want to ensure that you have a stable source of income and can afford the monthly mortgage payments, including the additional costs of the renovation.

Down Payment Requirements

Down payment requirements for rehab loans vary depending on the specific loan program and lender. Some programs, such as FHA 203(k) loans, allow for lower down payments compared to traditional mortgage loans.

However, be mindful that some lenders have overlays or more stringent eligibility requirements. It’s important to discuss the specific down payment requirements with your lender and ensure that you have the necessary funds available.

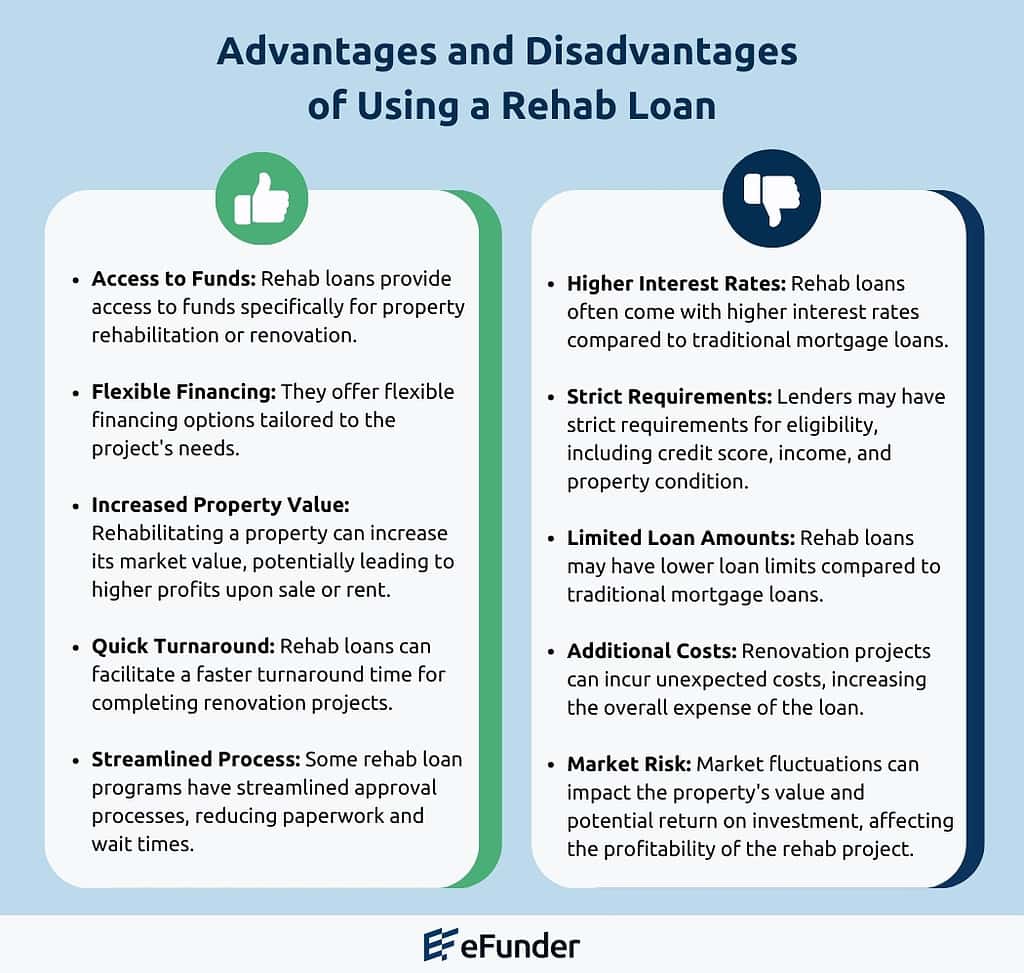

Advantages of Using a Rehab Loan

Rehab loans offer several advantages for homebuyers and homeowners looking to purchase or renovate a property. Let’s explore some of the key benefits:

Combining Purchase and Renovation Costs

One of the most significant advantages of rehab loans is the ability to combine the purchase price and renovation costs into a single loan. This means you can borrow the money needed to buy the property and cover the cost of necessary repairs or upgrades, all in one convenient package.

By financing both the purchase and renovation through a single loan, you can streamline the process and potentially save money on closing costs and interest rates compared to taking out separate loans.

Potential to Save Money

Conventional rehab loans can help you save money in the long run by allowing you to make necessary repairs and improvements upfront, rather than waiting and potentially facing more expensive issues down the road.

By investing in the property from the start, you can increase its value and potentially build equity more quickly. Plus, by financing the renovations through your mortgage, you can spread the costs over time and take advantage of potential tax benefits.

Improving Home Value

Rehab loans provide an opportunity to improve the value of your home from the moment you purchase it. By making strategic repairs and upgrades, you can enhance the property’s appeal and potentially increase its resale value in the current market.

Whether you’re planning to live in the home for years to come or considering it as an investment property, a rehab loan can help you maximize the potential of your purchase and set yourself up for future financial success.

Disadvantages of Rehab Loans

While rehab loans offer numerous benefits, it’s essential to consider the potential drawbacks before committing to this financing option. Here are some of the disadvantages to keep in mind:

Increased Paperwork and Documentation

Rehab loans often require additional paperwork and documentation compared to traditional mortgage loans. You’ll need to provide detailed plans for the renovation, including cost estimates, contractor bids, and a timeline for completion.

This extra documentation can be time-consuming and may require the assistance of professionals, such as architects or contractors, to ensure accuracy and compliance with lender requirements.

Higher Fees and Costs

Rehab loans may come with higher fees and costs compared to traditional mortgage loans. These can include origination fees, appraisal fees, and inspection fees, among others.

Additionally, interest rates for rehab loans may be slightly higher than those for traditional mortgages, as lenders perceive these loans as carrying a higher risk due to the added complexity of the renovation process.

Contractor Requirements and Approvals

Most rehab loans, including FHA 203(k) loans, require the use of licensed and approved contractors for the renovation work. This means you’ll need to find and vet contractors who meet the lender’s criteria and are willing to work within the guidelines of the loan program.

In some cases, you may need to hire a HUD consultant to oversee the renovation process and ensure compliance with the loan requirements. This added oversight can be beneficial but may also increase the overall cost and complexity of the project compared to a standard loan.

Rehab Loans for Real Estate Investors

If you’re a real estate investor looking to finance a fixer-upper, a rehab loan could be your golden ticket. These loans are designed to help you purchase and renovate an investment property, all in one tidy package.

Benefits for Investors

One of the biggest perks of rehab loans for real estate investors is the ability to finance both the purchase and renovation costs with a single loan. This streamlines the process and can save you time and money in the long run.

Plus, rehab loans often come with more flexible qualification requirements compared to traditional mortgages. This can be a game-changer for investors who may not have perfect credit or a ton of cash on hand for a down payment.

Financing Distressed Properties

Distressed properties, like foreclosures or short sales, can be a gold mine for investors. But they often need a lot of work to get them back in shape. That’s where rehab loans come in clutch.

With a rehab loan, you can finance the purchase of a distressed property and get the funds you need to make necessary repairs and upgrades. This can help you snag a great deal on a property and increase its value for resale or rental income.

Renovating Mixed-Use Properties

Rehab loans aren’t just for single-family homes. They can also be used to finance the renovation of mixed-use properties that combine residential and commercial spaces.

This can be a smart move for investors looking to diversify their portfolio and tap into the potential of up-and-coming neighborhoods. With a rehab loan, you can transform a dated mixed-use property into a modern, desirable space that attracts both residents and businesses.

In my experience of one of my client with eFunder, I’ve found that rehab loans are a viable alternative to hard money loans for investors. As I mentioned in a recent article on BiggerPockets, Most people are under the impression that if you’re an investor, the only option open to you is hard money. That’s not the case. Usually, you have to go outside the big lenders to get a renovation loan. I’ve seen many deals come through community banks, offering specialized loan products that benefit the neighborhood in the long term. Often, they prefer to see investors keeping the property as an investment rather than just flipping it. They typically require a 20% or more down payment and offer one mortgage that covers both construction and long-term financing with an interest rate of Prime +1, which is highly competitive compared to hard money.

– Terence Young

If you’re interested in learning more about the benefits of renovation loans and their comparison with hard money loans, check out the article from BiggerPockets: “Could Rehab Loans Replace Hard Money Loans for Investors?”

Conventional Rehab Loans vs. FHA 203(k) Loans

When it comes to rehab loans, you’ve got options. Two of the most common types are conventional rehab loans and FHA 203(k) loans. But what’s the difference? Let’s break it down.

Key Differences

Conventional rehab loans are typically offered by private lenders and have fewer restrictions on the type of property and renovation work that can be financed. They often have higher loan limits and more flexible qualification requirements, but may also come with higher interest rates.

On the flip side, FHA 203(k) loans are backed by the Federal Housing Administration and have more stringent guidelines for the property and renovation work. They typically have lower loan limits and require the borrower to occupy the property as their primary residence.

Eligibility Requirements

To qualify for a conventional rehab loan, borrowers generally need a higher credit score and a larger down payment compared to FHA 203(k) loans. Conventional loans may also have stricter debt-to-income ratio requirements.

FHA 203(k) loans, on the other hand, are designed to be more accessible to borrowers with lower credit scores and limited funds for a down payment. They also have more flexible debt-to-income ratio requirements, making them a good option for first-time homebuyers or those with less-than-perfect credit.

Renovation Restrictions

One of the key differences between conventional rehab loans and FHA 203(k) loans is the type of renovation work that can be financed. Conventional loans typically allow for a wider range of renovations, including luxury upgrades and cosmetic changes.

FHA 203(k) loans, on the other hand, have stricter guidelines for the type of renovations that can be financed. The work must focus on improving the safety, livability, and structural integrity of the property. Luxury upgrades and purely cosmetic changes may not be allowed.

Comparing Rehab Loans with Hard Money Loans

Flexibility and Affordability

While both rehab loans and hard money loans provide financing for property renovations, they differ significantly in terms of flexibility and affordability. Rehab loans typically offer more favorable terms, including lower interest rates and longer repayment periods, making them a preferred choice for investors seeking cost-effective solutions.

Accessibility

Rehab loans are accessible to a broader range of borrowers, including those with moderate credit scores and limited down payment capabilities. In contrast, hard money loans often require higher credit scores and substantial collateral, restricting access for some investors.

Long-Term Value

Investing in a property with a rehab loan allows you to create long-term value by improving its condition and increasing its market appeal. Hard money loans, while providing immediate funding, may not offer the same potential for value appreciation due to their shorter repayment terms and higher costs.

Understanding the Rehab Loan Process

Getting a rehab loan isn’t quite the same as getting a traditional mortgage. There are a few extra steps involved to make sure the renovation work goes smoothly and the property ends up in tip-top shape.

Application and Approval

The first step in getting a rehab loan is filling out an application with a lender who offers this type of financing. You’ll need to provide detailed information about your finances, the property you want to purchase, and the renovation work you plan to do.

The lender will review your application and determine if you qualify for the loan based on factors like your credit score, debt-to-income ratio, and the value of the property after renovation. If approved, you’ll receive a loan estimate outlining the terms of the loan.

Renovation Work and Inspections

Once you’ve closed on the loan and purchased the property, the real work begins. You’ll need to hire licensed contractors to complete the renovation work according to the plans and budget outlined in your loan agreement.

Throughout the renovation process, the lender will typically require periodic inspections to ensure the work is progressing as planned and meets quality standards. You may also need to provide the lender with updates and documentation along the way.

Closing and Payments

After the renovation work is complete and all inspections are passed, it’s time to close on the loan and start making payments. With a rehab loan, your monthly mortgage payment will include both the cost of the property and the cost of the renovations.

Keep in mind that rehab loans may come with higher interest rates and fees compared to traditional mortgages, so it’s important to factor these costs into your budget and long-term financial plan.

FAQs in Relation to What is Rehab Loan

What is a rehab loan and how does it work?

A rehab loan lets you buy and fix up a fixer-upper with one pot of money. It’s financing that covers both purchase price and renovation costs.

What are the cons of a 203k loan?

The 203k loan comes with more paperwork, strict contractor rules, and higher fees compared to standard loans.

Are rehab loans higher interest rates?

Yes, due to the added risk of funding renovations, rehab loans often have slightly higher interest rates than regular home loans.

What is the best loan for a rehabbing house?

FHA 203(k) loans are great for first-timers thanks to lower credit score requirements. Investors might prefer Fannie Mae’s HomeStyle Renovation Loan for flexibility.

Conclusion

So, what is a rehab loan? It’s a game-changer for anyone who wants to buy a fixer-upper. With a rehab loan, you can finance both the purchase price and the cost of renovations, all with one convenient loan.

Whether you’re a first-time homebuyer looking for a deal or an investor hoping to flip a property for profit, a rehab loan can help you achieve your goals. Just make sure you understand the requirements and work with a lender who has experience with this type of financing.

Ready to turn that diamond in the rough into your dream home? A rehab loan might be just the tool you need to make it happen.